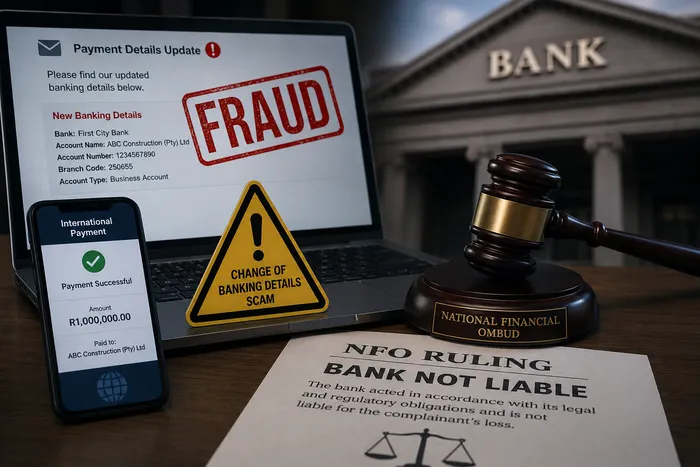

The National Financial Ombudsman (NFO) has dismissed a complaint against a bank over the fraudulent diversion of an international payment worth more than R1 million.

The NFO ruled that the bank acted in accordance with its legal and regulatory obligations and was not liable for the complainant’s loss.

The dispute arose after an international client attempted to pay the complainant for media and public relations services. However, the client fell victim to a change-of-banking-details scam after fraudsters intercepted email communications and substituted the complainant’s banking details with those of a fraudulent beneficiary account held at the bank.

As a result, the payment of more than R1 million was deposited into the fraudsters’ account instead of the complainant’s account.

The complainant argued that the bank failed to conduct proper due diligence when opening the fraudulent beneficiary’s account.

It was argued that the bank should have questioned the foreign payment, particularly because the beneficiary account had been recently opened, and the payment was for media and public relations services, while the beneficiary’s registered business was construction, which the complainant believed was an obvious mismatch.

The client said the bank was therefore negligent and should be held liable for the financial loss.

In its ruling, the NFO found that the funds had never been paid into the complainant’s bank account, meaning no bank-customer relationship existed between the complainant and the bank in relation to the disputed transaction. Consequently, the bank did not owe the complainant a duty of care in processing the payment.

The ombud further held that responsibility for the loss rested with the remitter, who had been deceived by the fraudulent banking details and remained responsible for ensuring that payment was made into the correct account.

The NFO also found that the bank had complied with all applicable regulatory requirements governing foreign payments, including the Financial Intelligence Centre (FIC) Act, the Currency and Exchanges Manual for Authorised Dealers (CEMAD), and standard due diligence procedures for inward international payments.

According to the ruling, the bank verified the beneficiary’s account name and account number, matched the invoice number with the remitter’s details, and confirmed the stated reason for the international payment.

The ombud found no evidence that the information available to the bank should reasonably have alerted it to possible fraud.

The complaint was dismissed, with the NFO concluding that the bank had acted appropriately and in compliance with its regulatory obligations. The ruling states that the complainant’s remedy lies against the remitter, whose debt to the complainant remains unpaid because the funds were transferred to the fraudulent account.